|

|

|

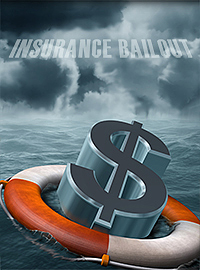

| Congress Poised to Bailout Insurers, Fleece Taxpayers |

|

|

By Betsy McCaughey

Wednesday, October 25 2017 |

Democrats and some Republicans in Congress are pushing for a $10 billion a year payout to insurance companies that sell Obamacare plans. President Trump calls it "bailing out" the insurance industry. Truer words were never spoken. The politicians backing this sweetheart deal claim it will protect consumers. Don't fall for it. The money will go straight to the bottom lines of insurers—who enjoy tremendous clout in Washington, D.C., thanks to over $85 million in campaign contributions and over $150 million spent on lobbying every year. The deal's authors, Sen. Lamar Alexander, R. Tenn., and Sen. Patty Murray, D. Wash., have taken hundreds of thousands in insurance contributions personally and through their PACs. No surprise the deal gives insurers everything they want: an estimated $10 billion a year cash plus $100 million in Obamacare ads. No other industry gets taxpayers to pay for their advertising. Meanwhile, consumers get nothing: no freedom to buy affordable plans without Washington-mandated benefits, no escape from onerous tax penalties for not enrolling. In 2010, the powerful insurance industry worked hand in glove with Democrats to enact the Affordable Care Act, a scheme compelling everyone to buy their product. The ACA also steered tens of billions of dollars in backdoor payments to insurers through 2016 to insulate them from losing their shirts on Obamacare. It doesn't get any sweeter—a law making your product mandatory and forcing taxpayers to subsidize your bottom line. The current $10 billion tug-of-war is more of the same—the Washington swamp exploiting the public. Insurers are fighting for more taxpayer largesse—and too many members of Congress are lining up to accommodate. But not President Trump. In the Rose Garden this week, Trump quipped that insurers "contribute massive amounts of money to political people. ... Me, I'm not interested in their money." The ACA requires insurers selling Obamacare plans to give low-income consumers a break on deductibles and copays. Insurers claim they lose money doing that, and want taxpayers to make up the shortfall. But Congress never voted for those payments, despite providing many others to the industry. No problem, under President Obama. He paid the insurers without getting Congress's consent. But the U.S. Constitution says the president can't spend what Congress doesn't appropriate. The House of Representatives sued and Obama lost. Federal judge Rosemary Collyer ruled that the payments were illegal. Fast forward to Oct. 12, when Trump announced he would halt the payments. Democrats howled that Trump was sabotaging the health law. Sen. Chris Murphy, D. Conn., accused the president of "health care arson," an inflammatory, untrue statement. Trump's decision lobs the issue back to Congress, where it belongs. But tragically that's where insurers have more sway than taxpayers. Denying it's a "bailout," Alexander claims "we have strong language in the Alexander-Murray agreement that consumers get the money, not the insurance companies." Those are weasel words. In truth, low-income consumers are already guaranteed breaks on copays and deductibles under the ACA. This agreement gives them nothing extra. The money is paid directly to insurers, going straight to profits. California Attorney General Xavier Becerra, one of 19 AGs trying to circumvent Judge Collyer's ruling by suing in the left-leaning Ninth Circuit, claims that without the payments, millions of families "would be left in the cold without coverage." Nonsense. The law guarantees low-income families insurance. What it does not do is guarantee insurers a profit. As for threats that without the payments, insurers will hike premiums, hurting consumers—don't buy that. State regulators have the final say on premiums. Of course, bailing out insurers will keep them participating in Obamacare, propping up the failing system. That's the Democrats' goal, to preserve Obama's legacy. But Republicans are fools to go along. It's pouring taxpayer money down the rat-hole. Why would lawmakers do that unless they're in bed with the insurance industry? Betsy McCaughey is a senior fellow at the London Center for Policy Research and a former lieutenant governor of New York State. |

Related Articles : |